Inventory management is the process of tracking, organizing, and controlling a company’s stock — whether it’s raw materials, components, or finished goods. At its core, it ensures you have the right products, in the right quantity, at the right time.

Done right, inventory management prevents stockouts, avoids overstocking, reduces waste, and keeps your supply chain moving smoothly.

What Is Inventory in Business?

Inventory refers to anything your business stores with the intention of selling, using in production, or delivering to customers. This includes:

- Raw materials (e.g. leather for shoes)

- Work-in-progress items (e.g. half-assembled products)

- Finished goods (e.g. packaged items ready to ship)

Inventory is a key business asset — but also a cost. Every item sitting on a shelf ties up cash. Managing it well keeps your operations lean and profitable.

What Is Inventory Management in Supply Chain?

In the broader supply chain, inventory management connects sourcing, warehousing, sales, and fulfillment. It helps ensure products flow efficiently from supplier to shelf to customer.

Key roles of inventory management in the supply chain:

- Balancing supply with demand

- Minimizing stockouts or overstock

- Keeping lead times low

- Avoiding production delays

In short, it keeps your supply chain predictable — even when demand isn’t.

What Is an Inventory Management System?

An inventory management system is the set of tools and processes used to track inventory levels, orders, sales, and deliveries. It can be as basic as a spreadsheet or as advanced as cloud-based software with real-time tracking and barcode scanning.

A good inventory management system helps you:

- Know what’s in stock (and where)

- Track incoming and outgoing items

- Set reorder points

- Forecast demand

- Manage multiple warehouses or channels

Cloud-based systems like Square, Katana, or TradeGecko integrate with POS, e-commerce, and accounting tools, automating most of the process.

For businesses needing physical warehousing and inventory support — not just software — logistics providers like Trebley offer flexible space, inventory control, and end-to-end order handling across Canada and the U.S..

What Is the First Step of Inventory Management?

The first step is stock identification and organization.

You need to:

- List all items in your inventory (raw materials, WIP, finished goods)

- Assign unique SKUs (stock keeping units)

- Organize items by category, location, and usage

- Choose a valuation method (e.g. FIFO, average cost)

Without this foundation, it’s impossible to track or optimize anything.

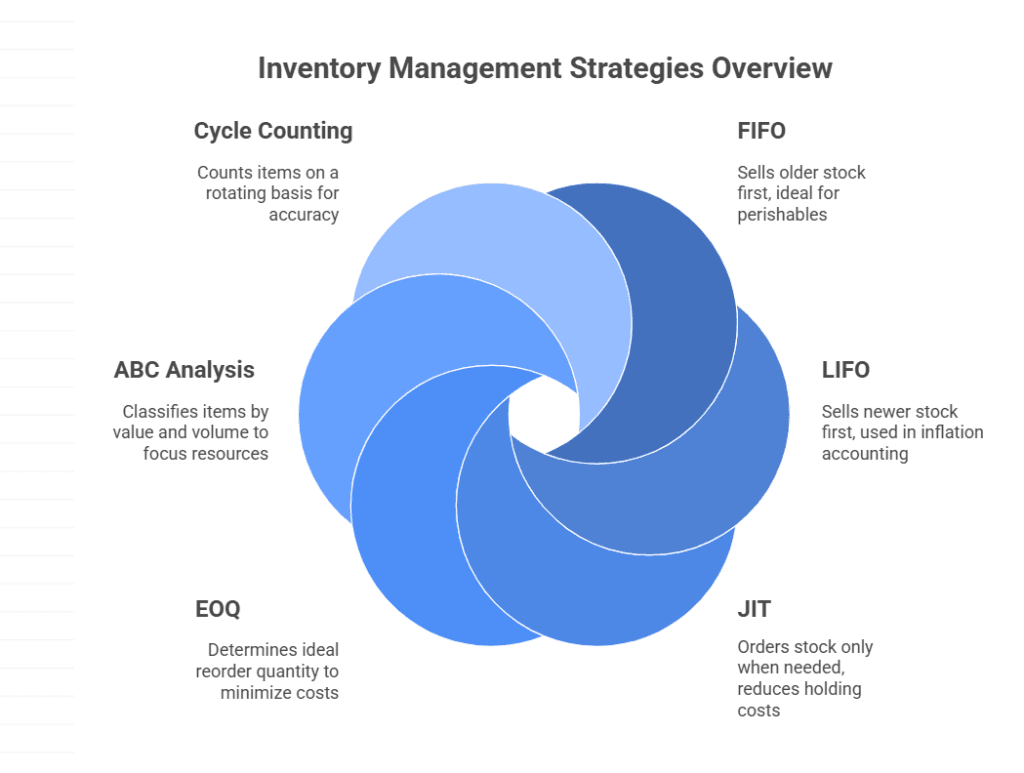

Common Inventory Management Methods

Most businesses use one or a combination of the following methods:

1. FIFO (First-In, First-Out)

This method ensures that the oldest stock (the first items you received) is sold or used first. It’s especially useful for perishable goods like food, cosmetics, or medicine, where older stock can expire or degrade. FIFO also helps maintain consistent product costs in your accounting records.

2. LIFO (Last-In, First-Out)

In this method, the most recently received inventory is sold first. While not ideal for perishables, LIFO can reduce taxable income during times of inflation by matching recent higher costs with current revenues. However, it’s banned under IFRS and not accepted in many countries outside the U.S.

3. Just-in-Time (JIT)

JIT means keeping inventory levels as low as possible and ordering only when needed. It reduces storage costs and frees up cash, but it requires precise demand forecasting and a very reliable supply chain. One small delay in delivery can halt production or sales.

4. EOQ (Economic Order Quantity)

EOQ uses a mathematical formula to calculate the ideal order quantity that minimizes the total cost of inventory — including ordering, holding, and stockout costs. It’s best for businesses with consistent demand and predictable lead times.

5. ABC Analysis

ABC analysis method sorts inventory into three categories based on their impact on overall costs:

- A items: High value, low quantity — need tight control and accurate forecasting

- B items: Moderate value and quantity — managed with balanced oversight

- C items: Low value, high quantity — require simpler controls

ABC analysis helps businesses focus their attention where it matters most.

6. Cycle Counting

Instead of shutting down operations for a full inventory audit, businesses count a portion of inventory on a regular schedule — daily, weekly, or monthly. This method is less disruptive and keeps inventory records accurate year-round.

Manual vs Automated Inventory Management

| Method | Manual Systems (e.g. spreadsheets) | Automated Systems (e.g. Square, Katana) |

| Accuracy | Prone to human error | Real-time, accurate data |

| Scalability | Hard to manage as business grows | Easy to scale across locations & channels |

| Efficiency | Time-consuming | Time-saving, often automated |

| Integration | Standalone | Syncs with sales, POS, fulfillment |

Manual systems might work for very small businesses, but as soon as you have multiple products, warehouses, or sales channels, software becomes essential.

Tips for Effective Inventory Management

- Forecast demand using historical data, seasonality, and market trends

- Set reorder points to avoid stockouts

- Use barcoding to reduce manual errors

- Audit your stock regularly (even with software)

- Avoid dead stock — discount or bundle items that haven’t moved in 6–12 months

- Prioritize high-value SKUs — don’t treat all inventory the same

- Track shrinkage from theft, damage, or misplacement

- Train your team on how to handle, log, and report inventory

Why Inventory Management Matters (With Examples)

- Retailers avoid lost sales by keeping bestsellers in stock

- Manufacturers ensure raw materials are ready for production

- E-commerce businesses can sync online and offline stock

- Wholesale distributors avoid over-ordering and holding costs

- Service-based businesses (e.g. salons) track product usage and reordering needs

Bad inventory management has real costs: lost customers, wasted stock, slow fulfillment, and tied-up capital.

Inventory isn’t just “stuff in a warehouse.” It’s one of your most valuable assets — and also a hidden cost center if not managed well.

Whether you’re a growing e-commerce brand or a multi-location retailer, getting inventory management right means:

- Lower costs

- Happier customers

- Faster growth

Start with clear organization, choose the right method for your needs, and use tools that grow with your business. If you need hands-on support, warehousing, or inventory handling in Canada or the U.S., companies like Trebley offer full-service logistics, from pick-and-pack to real-time inventory management — without long-term contracts.

Inventory Management FAQs

What is inventory management in simple terms?

It’s how businesses track what they have in stock, how much, and where it is — so they can meet demand and avoid waste.

How do small businesses manage inventory?

They often use software like Square, Katana, or spreadsheets (though those have limitations). Key steps include forecasting, auditing, and setting reorder points.

What is the difference between inventory management and stock control?

Stock control is one part of inventory management — focused specifically on keeping the right amount of stock. Inventory management is broader and includes planning, procurement, tracking, and analysis.

What is the goal of inventory management?

To balance supply and demand efficiently — ensuring customers get what they want, when they want it, without overstocking or running out.